When it comes to financial privacy, property rights protection and self-determination, it is well known that dark times have dawned. In the supposedly “free West”, bank accounts have recently been increasingly denied, closed or blocked for undesirable individuals. Commercial banks are being forced to act as detectives and stooges for the state in order to gather information and confiscate property. After all, normal tax revenue has long since ceased to be sufficient to finance the increasing excesses of highly indebted states.

Fiscal greed has led to extensive nationalization of the financial system and the worst is yet to come: the phase of increasing financial repression against ordinary citizens. It is no coincidence that the EU is now building up a complete asset register at breakneck speed.

To make matters worse, central banks around the world are now also starting to introduce CBDCs. Such a digital central bank currency would give the state possibilities that even the most unscrupulous rulers could only dream of until now.

If, for example, citizens are to travel less because of the climate and are no longer allowed to leave their city, CBDC money units could be programmed so that the money can only be spent in their own city. Is there too little consumption in the economy as a whole? Then the money is given an expiry date so that it can be spent more quickly. The government needs a few billion again to finance a new lockdown? Then – let’s say – 25 percent of everyone’s financial assets will be deducted without warning. There are no limits to the planned economy fantasies.

For citizens who no longer wish to participate in this imposition, the question arises as to how they can escape the dysfunctional state monetary system and the de facto nationalized banking system. After all, their own assets are foreseeably at risk: there is a threat of currency devaluation due to inflation and unannounced bail-ins. Cyprus showed the way a few years ago.

The possibility of saving one’s assets by fleeing into real assets, in particular physical precious metals such as gold and silver, is rightly pointed out time and again. However, today these tend to have the character of stores of value and are less suitable in physical form as an efficient means of payment in a globalized world. Another frequently discussed option is cryptocurrencies such as Bitcoin. Although they may be susceptible to price fluctuations and hacker attacks (especially if handled carelessly), they have the advantage that they can be sent quickly over long distances due to their digital nature.

The problem that cryptocurrencies have been struggling with since their inception and why they have never been able to seriously assert themselves against state alternatives has been a technological one (as well as a regulatory one, but let’s leave that part aside for now): the blockchain trilemma. This states that of the three important core properties of a blockchain – decentralization, security and scalability – at least one always falls by the wayside.

So-called proof-of-work cryptocurrencies such as Bitcoin generally have the advantage that they are decentralized and secure because there is no central authority that can manipulate and inflate the currency. The disadvantage is their low scalability. Bitcoin only manages seven transactions per second, which never comes close to Visa’s estimated 56,000 transactions. To tackle this problem of lack of scalability, the Lightning Network was placed on top of Bitcoin’s main layer, but this again leads to security problems because it means switching back and forth between the layers, creating new points of attack.

Proof-of-stake cryptocurrencies, on the other hand, can certainly compete with Visa in terms of scalability. But this comes at a price: they are organized as centralized entities that can ultimately control and manipulate the currency – also because a large proportion of the currency is often distributed to team members from the outset. Such cryptocurrencies give the state a central point of attack to regulate the currency out of existence. They are therefore insecure.

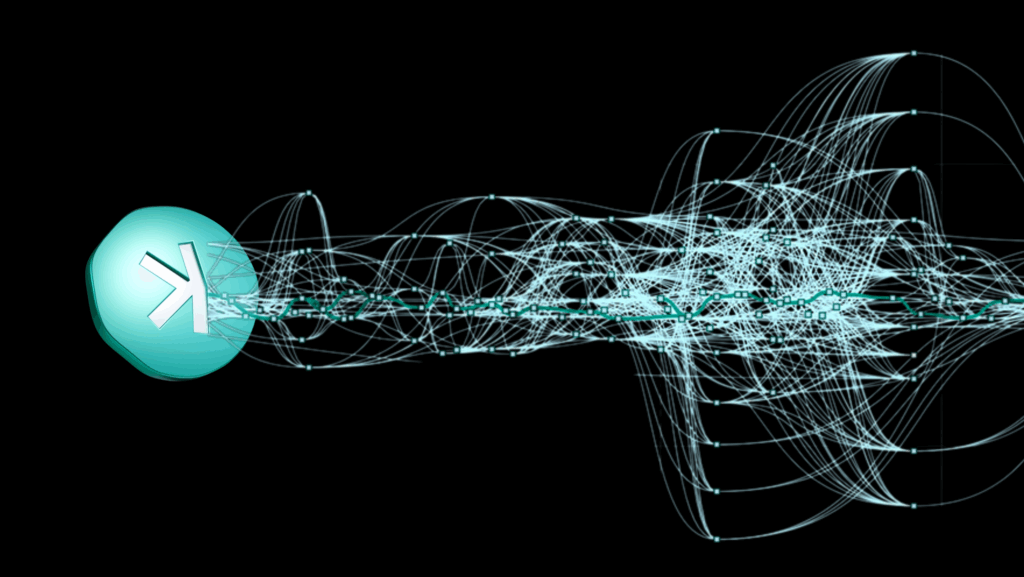

Apparently, however, there has now been a technical breakthrough that could solve the blockchain trilemma. Yonatan Sompolinsky, who is sometimes regarded as one of the possible inventors of Bitcoin, has been working with other developers for many years on the further technical development of blockchain technology. The result is the new block DAG technology, where “DAG” stands for Directed Acyclic Graph. Instead of a blockchain, the blocks are reorganized in a directed acyclic graph, enabling many more blocks and therefore transactions per second without compromising on security. You can see what such a block DAG looks like here:

This block DAG technology, in combination with various other innovations, has now resulted in a new cryptocurrency called Kaspa (KAS). Kaspa is not a company, but an open source project conceived by idealists, which is very reminiscent of Bitcoin. In fact, the Kaspa creators are avowed Bitcoin admirers. Even though Bitcoin has the “first mover advantage”, even die-hard Bitcoin fans now admit that Kaspa is superior in technical aspects. Some even joke that Bitcoin was just the test network for Kaspa. As the world’s fastest proof-of-work cryptocurrency, Kaspa offers everything at the same time: decentralization, security and scalability. The blockchain trilemma seems to have been solved.

While the speed of Bitcoin was still one block every 10 minutes, a Kaspa test network is currently running in which 10 blocks are generated per second, which is a new world record. The speed is to be gradually increased. There is talk of 100 blocks and more per second. If everything can be implemented as planned, Kaspa can easily compete with the giants of the credit card and banking industry. And all this without a central authority that could block accounts, manipulate the money supply and devalue the currency through inflation, because the money supply is capped at 28.7 billion KAS. The completely decentralized payment system can therefore not be shut down by any ruler, unless the entire Internet is paralyzed.

For those who value their financial freedom, the latest technological developments offer hope. Real alternatives to dysfunctional state money, which is susceptible to abuse of power, appear to be emerging on the horizon, which not only serve primarily as a store of wealth (like precious metals and Bitcoin), but also as a reliable, fast and secure payment system that is immune to manipulation by central banks and corporations. Human rights organizations and everyone who appreciate freedom should keep an eye on those developments.

Olivier Kessler

Olivier Kessler is the director of the Liberal Institute in Switzerland. This article was also published in German in “Finanz und Wirtschaft“.

This video explains in more detail how Kaspa solves the blockchain trilemma:

Here you can see arguments on the Bitcoin Lightning Network vs Kaspa debate:

Here is a video about the background of the Kaspa founder:

The Liberal Institute is delighted to hear from you.

LIBERALES INSTITUT

Scheideggstrasse 73

8038 Zürich, Schweiz

Tel.: +41 (0)44 364 16 66

institut@libinst.ch

INSTITUT LIBÉRAL

Boulevard de Grancy 19

1006 Lausanne, Suisse

Tel.: +41 (0)21 510 32 00

liberal@libinst.ch

ISTITUTO LIBERALE

Via Nassa 60

6900 Lugano, Svizzera

Tel.: +41 (0)91 210 27 90

liberale@libinst.ch

Receive information in German about current publications and events about once a month.